Starting January 1, 2016, Applicable Large Employers (ALEs) will face penalties for not offering coverage even if insurance is provided to full-time employees. The Patient Protection and Affordable Care Act (ACA) requires ALEs to offer coverage to substantially all full-time employees or pay a "no offer" penalty. The coverage requirement is 70 percent for 2015 for employers who meet the transition relief. Without further transition relief in sight, the percent covered requirement will increase to 95 percent.

'Full-time' status important to define

Many ALEs believe 95 percent of their full-time employees are offered coverage based on extending coverage to everyone who works 30 hours a week. However, ALEs may be surprised to find out after analyzing employee hours, the requirement isn't met. The reason for not meeting the requirement is because coverage is not offered to employees working full time part of the year, or full-time employees employed part of the year. In addition, ALEs may find themselves on the wrong side of these requirements for employees working full time only for four months. As these situations suggest, the definition of full-time status is critical.

Under the ACA, an employee's full-time status determination is based on a look-back measurement method or the default monthly measurement method. Under the monthly method, an employee is full time if they work 30 hours a week multiplied by the number of weeks in the month. To meet the requirement, 95 percent of full-time employees for each month must be offered coverage. The look-back method measures hours over a three- to 12-month measurement period to determine full-time status. This status is locked in over a corresponding stability period. ALEs using the look-back method will know with greater certainty who is full time and should be offered coverage, thereby minimizing the risk of being assessed a "no offer" penalty on top of providing coverage. For those not offering coverage, the look-back method provides greater clarity on potential penalties, if any.

Benefit of the Look-Back Method

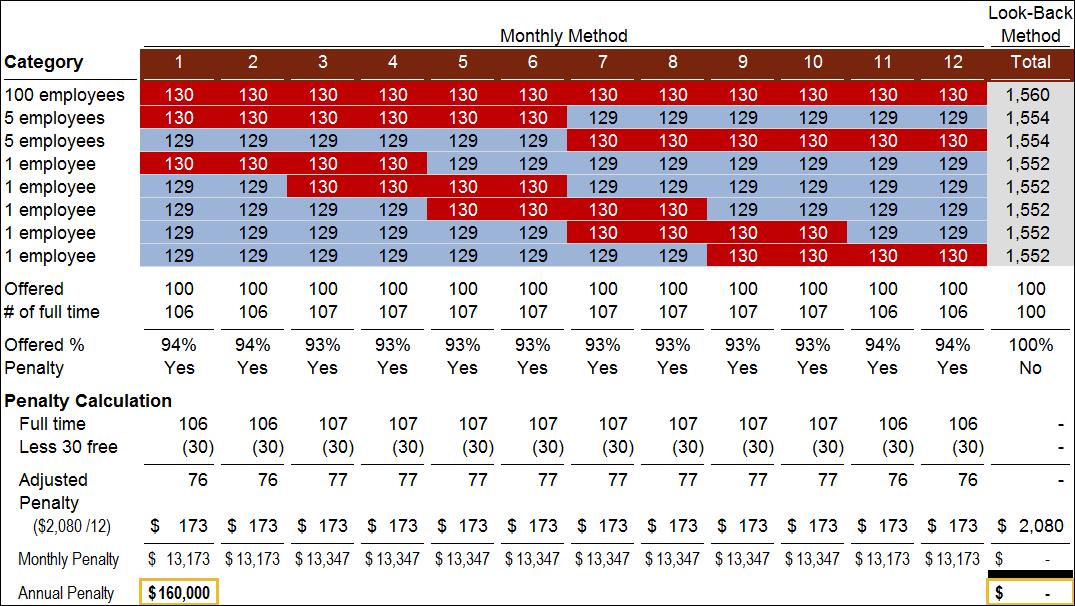

The following example illustrates the benefit of the look-back method for ongoing employees outside of their initial measurement period. ABC Company has 115 employees on staff: 100 employees working 130 hours a month for 12 months (130 hours a month is considered full time), five employees working full time for months one through six, five employees working full time for months seven through 12, and five employees full time at a four-month increment throughout the year. ABC Company offered coverage to the first 100 employees working 130 hours a month throughout the year:

The example below shows that under the monthly method, ABC Company is offering coverage to less than 95 percent of their full-time employees for all 12 months and may be assessed the "no offer" penalty each month. The penalty is $173.33 per month ($2,080 annually) multiplied by the number of full-time employees, less the 30 (this number is 80 for 2015 only) full-time employees. ABC Company could have a $160,000 non-deductible penalty for not offering coverage to 95 percent of its employees, even though ABC Company offered coverage to 100 full-time employees. Click the image to enlarge.

If ABC Company used the look-back method, it would know which employees are full time, offer coverage to those employees, and would incur no penalty. By using a 12-month look-back period, ABC Company would meet the 95 percent test without extending coverage to any other employees because they would be classified as part time. As a result, ABC Company would not extend coverage to any more employees and would save $160,000 in non-deductible penalties by using the look-back method.

Be Aware of the Risk

Organizations should be aware of this risk before it's too late. Many ALEs offer health insurance, which is not only a significant cost to the organization, but also a significant benefit to their employees. By not taking advantage of the look-back method, organizations may be exposed to "no offer" penalties whether the organization offers health insurance or not.