Despite a somewhat lackluster April and May, equities markets ended one of the better first halves of a year in quite some time by the end of June. The Nasdaq, S&P 500, and Dow were up 32.32%, 16.89%, and 4.94% for the year, respectively. It was the Nasdaq’s best first half of a year since 1983, primarily due to growth in tech stocks driven by the surge in AI.

Market participants have become more confident that the economy is strong enough to shrug off the historic pace of rate hikes, banking system troubles, and stubborn inflation data. However, that suggests the Fed will have to keep rates higher for a more extended period and bond markets sold off.

Returns % as of 6/30/23

Index

1 MO

QTD

YTD

1 YR

3 YR

5 YR

10 YR

US Equity

S&P 500 TR USD

6.61

8.74

16.89

19.59

14.60

12.31

12.86

DJ Industrial Average TR USD

4.68

3.97

4.94

14.23

12.30

9.59

11.26

NASDAQ Composite TR USD

6.65

13.05

32.32

26.14

11.94

13.93

16.21

International Developed Markets

MSCI World ex USA NR USD

4.75

3.03

11.29

17.41

9.30

4.58

5.40

Emerging Markets Equity

MSCI EM NR USD

3.80

0.90

4.89

1.75

2.32

0.93

2.95

US Fixed Income

BBgBarc US Agg Bond TR USD

-0.36

-0.84

2.09

-0.94

-3.96

0.77

1.52

Global Fixed Income

BBgBarc Global Aggregate TR USD

-0.01

-1.53

1.43

-1.32

-4.96

-1.09

0.20

Source: Morningstar. Past performance does not guarantee future results. All data is from sources believed to be reliable but cannot be guaranteed or warranted. Please see disclosure at the end of commentary for limitations to index performance.

Equities

The market’s narrow rally of the first half, dominated by a handful of tech stocks, broadened in June.

The Nasdaq finished up over 30% YTD for its best first half in 40 years, while the S&P 500 had its best first half since 2019.

Market breadth turned strongly positive in June.

All 11 sectors of the S&P were up for the month, led by Consumer Discretionary (+12.07%), while Information Technology led for the half (+42.77%).1

Fixed Income

Yields rebounded in June as strains from bank failures and the debt-ceiling crisis eased.

Futures markets have traders pricing in an 87% chance of the Fed raising rates in July, and the target rate will finish the year above current levels (i.e., no rate cuts).

Expectations of ongoing rate increases in the near future have floated the short end of the curve, with the two-year moving up 50 bps in June.

The two-year to 10-year yield curve hit its deepest inversion since 1981.2

Factors

As usual, returns associated with risk factors have been a mixed bag. In the United States, both size and momentum outperformed for the month of June; while in international developed markets, value and momentum led; and in emerging markets, value and size have continued to outperform.3

News Impacting Markets

The Economy, Inflation, and The Fed

Resilient economic data (stronger than anticipated growth coupled with historically low unemployment) has reignited talk of a potential “soft landing.” Meanwhile, headline inflation continues to cool slowly, but core prices, which exclude food and energy, have remained sticky. The Fed’s preferred inflation gauge, the core personal consumption expenditures price index (PCE), increased in May by 4.6% from a year earlier. This almost assures that the Fed will pick up from June’s interest-rate hike pause with several more rate increases starting in July.4

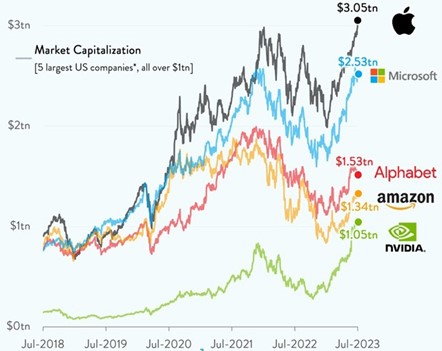

Tech Giants Have Roared…But the Rest of the Market May Finally Be Catching Up

Until June, the largest tech companies by size were responsible for most of the stock market’s 2023 gains. Alphabet (Google), Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla have all experienced a significant surge in their share prices. Apple closed the month of June with a share price that made it the first company in history to be valued at over $3 trillion, while Nvidia’s shares have tripled in six months, propelling them into $1 trillion club. However, the June equity market rally was broad-based. Shares of 454 companies in the S&P 500 were up, with 155 up at least 10%. The rally also expanded to include mid- and small-cap stocks and equities from international and emerging markets.5

Source: Chartr, Koyfinr. Past performance does not guarantee future results. All data is from sources believed to be reliable but cannot be guaranteed or warranted.

The whiplash investors have experienced, from the exceedingly poor performance across stock and bond markets in 2022 to the healthy rebound in the first half of 2023, is a study of the benefits of being a patient investor. Time and again, we see studies that point to the “average” performance of investors lagging behind the performance of the markets. Much of the root cause of that underperformance is attributable to investors making the wrong move at the wrong time—either chasing good performance or fleeing from bad.

What does the second half of 2023 hold for investors? No one knows. But we do know that over time markets reward patience.

Questions about what market performance means for your portfolio? We can help.